I've moved the three posts responding to Matt's posting to the Russia thread.

http://generationaldynamics.com/forum/v ... 2481#p2481

John

Financial topics

Kaplan thinks we are due for major move higher

I just went long again. Note that PPI showed “surprise” inflation today, CRB rallied 2%. Treasuries have been selling off hard (these are all bullish signals). Finally, look at whole foods today, up 37% - that’s a monster move, what was the news? Basically nothing, their quarter was horrible, sales are down, store traffic is down, the stock was down 75% over the last year, and yet it rises 37% today after an analyst upgrade?? That may or may not be important, but it should tell you a little bit about market psychology and where we are right now…

At this point we are just 70 points away from a brand spankin’ new low on the DOW – the best thing that could happen tomorrow is that we break though to new lows, emboldening the chart fools to sell – that will mark an important short term bottom and the start of a major rally. You couldn’t ask for a better setup.

___________________________Kaplan___________________

U.S. Treasuries continued their sharp retreat. This confirms beyond a shadow of a doubt that the great asset shift of 2009 has begun.

So far, a lot of the money which has left U.S. Treasuries has gone into money-market funds and other safe-haven time deposits instead of into equities. But people will not accept 1% gross returns indefinitely, so most of this money will find its way into the stock market. Many people don’t want to be among the first to buy, so they’ll pile in once we’ve already enjoyed a rebound of 20% or 30%.

Of course, the financial markets will appropriately punish the huge number of poorly-informed investors who decided to “reduce their risk” since October by selling equities when they should have been following corporate insiders and buying them aggressively.

The U.S. dollar also failed to surpass its double top. Both U.S. Treasuries and the U.S. dollar have been a reliable leading tandem of the global financial markets for several decades. Declining interest in these safe-haven assets will soon translate into a huge appetite for higher-risk assets.

While gold-mining shares retreated moderately, numerous funds of energy shares were higher including my personal favorites RSX, KOL, and FCG.

Another rare contrarian comments on the oddity of finding so little company when buying low or selling high:

http://seekingalpha.com/article/121395- ... nvironment

Fantasy versus reality in the residential housing market: When you learn to tell the difference between what is real and what is phony, it becomes quickly apparent that the housing bubble still has a long way to collapse:

http://online.wsj.com/article/SB123448313158279827.html

In the above link, a woman is renting a Seattle waterfront home for $10,000 per month. This house is allegedly worth 15 million dollars.

Let’s think about this for a moment. $10,000 per month is $120,000 per year. That’s equal to just 0.8% of $15 million!

This is about one tenth the average historic annual rental rate of 8%, going back a century or more. So this means that the house is really worth close to $1.5 million, not $15 million.

Once everyone realizes that housing prices are only really worth what they can be rented for, multiplied by an appropriate factor, then either rents have to soar or prices have to plunge.

It’s not rents which will rise. When a property is rented, the agreement between a landlord and a tenant represents the intersection of actual supply with true demand. Rents are reality. Housing prices are fantasy, and will soon have to decline sharply to catch up with rental valuations.

The financial media have no concept of asset interrelationships. This makes it difficult for most investors to understand the critical interactions between different kinds of securities.

For example, there has been a lot of nonsense about how investors are allegedly buying gold and gold mining shares in response to tightening credit conditions and concerns over a worsening global recession.

Nothing could be further from the truth. When the global economy is contracting, precious metals will plummet even more than the broader equity market. As the S&P 500 retreated by half in 2007-2008, GDX (an exchange-traded fund of gold mining shares) plunged more than 72% over an even shorter time span.

The four-month rally in gold and its shares since October 24 is sending exactly the opposite message: the global economy is about to powerfully rebound. Gold is simply serving in its familiar role as a leading indicator of this turnaround.

Beginning on November 20 and 21, 2008, which is about four weeks after gold mining shares began to move higher, energy shares have been forming a bullish pattern of higher lows. Like gold mining shares, they are sending a message that the world is not headed for a deflationary depression, as the media would have you believe, but a highly inflationary period of global growth.

Beginning in the second week of December 2008, high-yield corporate bonds have been confirming the exact same message by rebounding sharply from 75-year lows.

Very few analysts will talk about a highly inflationary period of global growth—especially on a day when the Dow Jones Industrial Average slumped to its lowest point since March 2003. This new Dow low, which was not confirmed by other major equity indices, is a perfect excuse for amateurs to sell in fear while insiders have yet another opportunity to enjoy wonderful bargains.

The media are hell bent on driving with their eyes firmly in the rear-view mirror. They have a great viewpoint on where we’ve been, but not the faintest clue as to where we’re going.

I’ve heard all kinds of commentators give the most convoluted reasons why U.S. Treasuries and other global government bonds have been slumping since December 30, 2008. The simplest and most obvious explanation—that inflation is set to surge sharply higher, and that government bonds are therefore signaling this in advance as they have done for centuries—is dismissed since analysts can’t envision a resurgence of high inflation after about 26 years of low inflation.

If I walk down the street and I see a candy wrapper on the ground, then I assume someone ate a candy bar and discarded the wrapper. I can invent several dozen alternative explanations, but the clearest one is almost surely the truth.

There are different kinds of investors in different kinds of securities. You’ll rarely see an amateur investor bragging to his friends about his latest U.S. Treasury purchase—even during the fourth-quarter 2008 bubble. Government bonds are bought and sold mostly by pension funds and other major institutions, rather than by individuals. Trading in this sector therefore tends to be dominated by wealthy investors who are usually several weeks ahead of the general public.

The same is true of the U.S. dollar. While currency trading has become somewhat better known among the public, it is still primarily the realm of well-heeled multinational corporations.

High-yield corporate bonds also are not widely held or traded by most people, or discussed often in the media. There was incredible hype when these bonds collapsed in the autumn of 2008—and almost zero coverage of their impressive recovery this winter.

Gold mining shares have a sort of cult following, but the public tends to be relatively ignorant of them also.

Therefore, when you see U.S. Treasuries plummeting, and the U.S. dollar struggling to set a new three-year high, while gold mining shares have more than doubled in slightly less than four months, and high-yield corporate bonds have rebounded significantly from their lows, then the combined message of all of these actions is that the global economy is preparing for a recovery.

The key word here is “preparing”. The financial markets usually lead the real economy by about six to nine months. Therefore, when you hear stories about how this or that segment of Main Street continues to deteriorate, this has already been fully anticipated by the 2008 collapse and has zero relevance to the future of the financial markets.

Asset valuations are therefore telling you today what is going to happen in the summer and autumn of 2009.

The lagging behavior of equities is common behavior—and very fortunate behavior if you are a contrarian.

Let’s go back to the summer of 2008—exactly six months ago (August 19, 2008)--and see what was happening at that time.

U.S. Treasuries had been rallying for several weeks. The U.S. dollar had been surging higher for several weeks. Gold mining shares had been slumping badly for five months, while energy shares had recently joined in with a sharp pullback of their own. In every way, it was a nearly perfect inverse image of what we have today.

Did anyone in the media in August 2008 therefore conclude that the global economy was setting up for a major contraction (besides a tiny minority, of course)?

They did not—at least 98% of them did not--because the stock market was generally strong over the same period of time. The media made the same mistake six months ago that they are making now: they concluded that since the stock market was rallying, it would continue to move higher.

The biggest mistake most amateur investors make is to project the recent past into the indefinite future.

If they media had even the faintest idea of how various assets correlate with each other, then they would have understood last August that the one-two punch of rising U.S. Treasuries and a rising U.S. dollar, combined with slumping gold mining shares, could have only one implication: a significant pullback in the stock market and in commodities. Since we had experienced so many bubbles in 2007-2008, this pullback was likely to be noticeably more severe than usual—as of course it proved to be last autumn.

All of this, of course, was detailed rather meticulously if you review my daily updates from last summer and early autumn. Some other analysts, too, deserve credit for making similarly accurate observations. This hardly required any great skill—simply recognizing that patterns which had proven reliable for centuries would continue to be valid.

Since we have had virtually an exact reversal in asset behavior today as compared with a half year ago, the outcome over the next several months will be the exact opposite of what we experienced after August 2008: enormously higher equity prices over the next half year; sharply rising commodities; surging commodity-share valuations; a new all-time low for the U.S. dollar index; plummeting government bonds worldwide; soaring global inflation; surprising growth in all regions; and an end to recessions throughout the “real” economy on a worldwide basis before the end of 2009.

Almost everyone recognizes patterns in the weather. If it suddenly gets sharply colder in February in the Northern Hemisphere, no one concludes that we won’t have summer, or that there will be even more snow in July and August.

Although the financial markets are not quite as reliable as seasonal weather patterns, a proven sequence of events which has resulted in the same pattern of future behavior on a hundred occasions in the past few centuries will likely exhibit the exact same behavior pattern this year, and next year, and the year after, and so on.

It is no coincidence, either, that commodity shares have been consistently outperforming the broader market. Whenever this has happened in past decades, it has signaled that inflation will be an even more significant factor than growth in the “real” economy six to nine months in the future.

Most amateur investors act with blinders. Chart slaves make the same mistake: they look at a chart of something like the S&P 500 in isolation and conclude that this or that is going to occur, without studying the overall picture.

To stick with the automobile analogy, that’s better than driving with your eyes firmly in the rear-view mirror—but if you only look in the front windshield and ignore your mirrors entirely, then that is still a dangerous way to move through heavy traffic.

Just as an intelligent driver has to be fully aware of nearby drivers to be maximally safe, you have to be knowledgeable of the interrelationships between various financial assets to form an accurate viewpoint of what is going to happen in the future.

There are times when the future of the financial markets is relatively fuzzy, and times when it is crystal clear. When it is fuzzy, it is usually best not to act. This happens when different assets are sending conflicting signals, as is sometimes the case.

Today, however, there is essentially no ambiguity. The message of the great asset shift of 2009 could hardly be clearer. Those assets which always tell you loudly and most clearly what is going to happen are currently shouting at the top of their lungs. While the vast majority of investors are acting as though they are deaf, heed these cries and purchase the most compelling equity funds now before they enjoy their strongest short-term rise in several decades.

Take care.

At this point we are just 70 points away from a brand spankin’ new low on the DOW – the best thing that could happen tomorrow is that we break though to new lows, emboldening the chart fools to sell – that will mark an important short term bottom and the start of a major rally. You couldn’t ask for a better setup.

___________________________Kaplan___________________

U.S. Treasuries continued their sharp retreat. This confirms beyond a shadow of a doubt that the great asset shift of 2009 has begun.

So far, a lot of the money which has left U.S. Treasuries has gone into money-market funds and other safe-haven time deposits instead of into equities. But people will not accept 1% gross returns indefinitely, so most of this money will find its way into the stock market. Many people don’t want to be among the first to buy, so they’ll pile in once we’ve already enjoyed a rebound of 20% or 30%.

Of course, the financial markets will appropriately punish the huge number of poorly-informed investors who decided to “reduce their risk” since October by selling equities when they should have been following corporate insiders and buying them aggressively.

The U.S. dollar also failed to surpass its double top. Both U.S. Treasuries and the U.S. dollar have been a reliable leading tandem of the global financial markets for several decades. Declining interest in these safe-haven assets will soon translate into a huge appetite for higher-risk assets.

While gold-mining shares retreated moderately, numerous funds of energy shares were higher including my personal favorites RSX, KOL, and FCG.

Another rare contrarian comments on the oddity of finding so little company when buying low or selling high:

http://seekingalpha.com/article/121395- ... nvironment

Fantasy versus reality in the residential housing market: When you learn to tell the difference between what is real and what is phony, it becomes quickly apparent that the housing bubble still has a long way to collapse:

http://online.wsj.com/article/SB123448313158279827.html

In the above link, a woman is renting a Seattle waterfront home for $10,000 per month. This house is allegedly worth 15 million dollars.

Let’s think about this for a moment. $10,000 per month is $120,000 per year. That’s equal to just 0.8% of $15 million!

This is about one tenth the average historic annual rental rate of 8%, going back a century or more. So this means that the house is really worth close to $1.5 million, not $15 million.

Once everyone realizes that housing prices are only really worth what they can be rented for, multiplied by an appropriate factor, then either rents have to soar or prices have to plunge.

It’s not rents which will rise. When a property is rented, the agreement between a landlord and a tenant represents the intersection of actual supply with true demand. Rents are reality. Housing prices are fantasy, and will soon have to decline sharply to catch up with rental valuations.

The financial media have no concept of asset interrelationships. This makes it difficult for most investors to understand the critical interactions between different kinds of securities.

For example, there has been a lot of nonsense about how investors are allegedly buying gold and gold mining shares in response to tightening credit conditions and concerns over a worsening global recession.

Nothing could be further from the truth. When the global economy is contracting, precious metals will plummet even more than the broader equity market. As the S&P 500 retreated by half in 2007-2008, GDX (an exchange-traded fund of gold mining shares) plunged more than 72% over an even shorter time span.

The four-month rally in gold and its shares since October 24 is sending exactly the opposite message: the global economy is about to powerfully rebound. Gold is simply serving in its familiar role as a leading indicator of this turnaround.

Beginning on November 20 and 21, 2008, which is about four weeks after gold mining shares began to move higher, energy shares have been forming a bullish pattern of higher lows. Like gold mining shares, they are sending a message that the world is not headed for a deflationary depression, as the media would have you believe, but a highly inflationary period of global growth.

Beginning in the second week of December 2008, high-yield corporate bonds have been confirming the exact same message by rebounding sharply from 75-year lows.

Very few analysts will talk about a highly inflationary period of global growth—especially on a day when the Dow Jones Industrial Average slumped to its lowest point since March 2003. This new Dow low, which was not confirmed by other major equity indices, is a perfect excuse for amateurs to sell in fear while insiders have yet another opportunity to enjoy wonderful bargains.

The media are hell bent on driving with their eyes firmly in the rear-view mirror. They have a great viewpoint on where we’ve been, but not the faintest clue as to where we’re going.

I’ve heard all kinds of commentators give the most convoluted reasons why U.S. Treasuries and other global government bonds have been slumping since December 30, 2008. The simplest and most obvious explanation—that inflation is set to surge sharply higher, and that government bonds are therefore signaling this in advance as they have done for centuries—is dismissed since analysts can’t envision a resurgence of high inflation after about 26 years of low inflation.

If I walk down the street and I see a candy wrapper on the ground, then I assume someone ate a candy bar and discarded the wrapper. I can invent several dozen alternative explanations, but the clearest one is almost surely the truth.

There are different kinds of investors in different kinds of securities. You’ll rarely see an amateur investor bragging to his friends about his latest U.S. Treasury purchase—even during the fourth-quarter 2008 bubble. Government bonds are bought and sold mostly by pension funds and other major institutions, rather than by individuals. Trading in this sector therefore tends to be dominated by wealthy investors who are usually several weeks ahead of the general public.

The same is true of the U.S. dollar. While currency trading has become somewhat better known among the public, it is still primarily the realm of well-heeled multinational corporations.

High-yield corporate bonds also are not widely held or traded by most people, or discussed often in the media. There was incredible hype when these bonds collapsed in the autumn of 2008—and almost zero coverage of their impressive recovery this winter.

Gold mining shares have a sort of cult following, but the public tends to be relatively ignorant of them also.

Therefore, when you see U.S. Treasuries plummeting, and the U.S. dollar struggling to set a new three-year high, while gold mining shares have more than doubled in slightly less than four months, and high-yield corporate bonds have rebounded significantly from their lows, then the combined message of all of these actions is that the global economy is preparing for a recovery.

The key word here is “preparing”. The financial markets usually lead the real economy by about six to nine months. Therefore, when you hear stories about how this or that segment of Main Street continues to deteriorate, this has already been fully anticipated by the 2008 collapse and has zero relevance to the future of the financial markets.

Asset valuations are therefore telling you today what is going to happen in the summer and autumn of 2009.

The lagging behavior of equities is common behavior—and very fortunate behavior if you are a contrarian.

Let’s go back to the summer of 2008—exactly six months ago (August 19, 2008)--and see what was happening at that time.

U.S. Treasuries had been rallying for several weeks. The U.S. dollar had been surging higher for several weeks. Gold mining shares had been slumping badly for five months, while energy shares had recently joined in with a sharp pullback of their own. In every way, it was a nearly perfect inverse image of what we have today.

Did anyone in the media in August 2008 therefore conclude that the global economy was setting up for a major contraction (besides a tiny minority, of course)?

They did not—at least 98% of them did not--because the stock market was generally strong over the same period of time. The media made the same mistake six months ago that they are making now: they concluded that since the stock market was rallying, it would continue to move higher.

The biggest mistake most amateur investors make is to project the recent past into the indefinite future.

If they media had even the faintest idea of how various assets correlate with each other, then they would have understood last August that the one-two punch of rising U.S. Treasuries and a rising U.S. dollar, combined with slumping gold mining shares, could have only one implication: a significant pullback in the stock market and in commodities. Since we had experienced so many bubbles in 2007-2008, this pullback was likely to be noticeably more severe than usual—as of course it proved to be last autumn.

All of this, of course, was detailed rather meticulously if you review my daily updates from last summer and early autumn. Some other analysts, too, deserve credit for making similarly accurate observations. This hardly required any great skill—simply recognizing that patterns which had proven reliable for centuries would continue to be valid.

Since we have had virtually an exact reversal in asset behavior today as compared with a half year ago, the outcome over the next several months will be the exact opposite of what we experienced after August 2008: enormously higher equity prices over the next half year; sharply rising commodities; surging commodity-share valuations; a new all-time low for the U.S. dollar index; plummeting government bonds worldwide; soaring global inflation; surprising growth in all regions; and an end to recessions throughout the “real” economy on a worldwide basis before the end of 2009.

Almost everyone recognizes patterns in the weather. If it suddenly gets sharply colder in February in the Northern Hemisphere, no one concludes that we won’t have summer, or that there will be even more snow in July and August.

Although the financial markets are not quite as reliable as seasonal weather patterns, a proven sequence of events which has resulted in the same pattern of future behavior on a hundred occasions in the past few centuries will likely exhibit the exact same behavior pattern this year, and next year, and the year after, and so on.

It is no coincidence, either, that commodity shares have been consistently outperforming the broader market. Whenever this has happened in past decades, it has signaled that inflation will be an even more significant factor than growth in the “real” economy six to nine months in the future.

Most amateur investors act with blinders. Chart slaves make the same mistake: they look at a chart of something like the S&P 500 in isolation and conclude that this or that is going to occur, without studying the overall picture.

To stick with the automobile analogy, that’s better than driving with your eyes firmly in the rear-view mirror—but if you only look in the front windshield and ignore your mirrors entirely, then that is still a dangerous way to move through heavy traffic.

Just as an intelligent driver has to be fully aware of nearby drivers to be maximally safe, you have to be knowledgeable of the interrelationships between various financial assets to form an accurate viewpoint of what is going to happen in the future.

There are times when the future of the financial markets is relatively fuzzy, and times when it is crystal clear. When it is fuzzy, it is usually best not to act. This happens when different assets are sending conflicting signals, as is sometimes the case.

Today, however, there is essentially no ambiguity. The message of the great asset shift of 2009 could hardly be clearer. Those assets which always tell you loudly and most clearly what is going to happen are currently shouting at the top of their lungs. While the vast majority of investors are acting as though they are deaf, heed these cries and purchase the most compelling equity funds now before they enjoy their strongest short-term rise in several decades.

Take care.

Re: Kaplan thinks we are due for major move higher

Dear Gordo,

Whoever wrote this is living in the past. People have changed. New

generational dynamics have taken over, and the world this paragraph

describes no longer exists. As they say, it's Gone with the Wind.

People today are not buying cars, they're not drinking Starbucks

coffee, and they're not buying stocks. To people today, and for

years and decades to come, making 1% gross returns is infinitely

better than continuing to lose principal.

The stock market crash still has a long way down to go.

** Market reaches a 'crisis low' as east European banks raise widespread concern

** http://www.generationaldynamics.com/cgi ... 20#e090220

Sincerely,

John

We've been hearing this for months now, and it's never happened.Gordo wrote: > So far, a lot of the money which has left U.S. Treasuries has gone

> into money-market funds and other safe-haven time deposits instead

> of into equities. But people will not accept 1% gross returns

> indefinitely, so most of this money will find its way into the

> stock market. Many people don’t want to be among the first to buy,

> so they’ll pile in once we’ve already enjoyed a rebound of 20% or

> 30%.

Whoever wrote this is living in the past. People have changed. New

generational dynamics have taken over, and the world this paragraph

describes no longer exists. As they say, it's Gone with the Wind.

People today are not buying cars, they're not drinking Starbucks

coffee, and they're not buying stocks. To people today, and for

years and decades to come, making 1% gross returns is infinitely

better than continuing to lose principal.

The stock market crash still has a long way down to go.

** Market reaches a 'crisis low' as east European banks raise widespread concern

** http://www.generationaldynamics.com/cgi ... 20#e090220

Sincerely,

John

Re: Kaplan thinks we are due for major move higher

I completely agree that the market has a long way to go on the downside, I just don't think it will happen the way you seem to expect.John wrote:Whoever wrote this is living in the past. People have changed. New

generational dynamics have taken over, and the world this paragraph

describes no longer exists. As they say, it's Gone with the Wind.

People today are not buying cars, they're not drinking Starbucks

coffee, and they're not buying stocks. To people today, and for

years and decades to come, making 1% gross returns is infinitely

better than continuing to lose principal.

The stock market crash still has a long way down to go.

This statement: "People today are not buying cars, they're not drinking Starbucks

coffee, and they're not buying stocks" is really not true at all. Its more like 5-10% of the population have seriously pulled back. This alone is enough to produce a severe recession (which it has done) but the vast majority have not woken up to the reality of the situation yet, and they may not for a while longer. A friend wrote yesterday from Boston:

> As for the general economy, I am absolutely appalled at what I see

> around me. NOBODY is cutting back. Restaurants in Boston area packed

> on a Tuesday night. Girlfriend's brother just bought a used Harley

> for $8k....he already has a bike, muscle car, new hot tub, new

> hardwood floors, new 52" TV, all new guitar collection....all of it

> financed (He probably makes $60k and has no savings- and he's not a

> dumb guy at all).

> Single mom I know making 45k buying her 9 yr old a laptop....everyone

> is planning a vacation in the bahamas. I see full blown denial /

> "what the hell, I'm in this deep, no sense trying to change things now"

I see the same sort of thing. If (when?) everyone really cuts back, that’s when the economy truly goes to hell in a hand basket. I don’t see this happening right now at all where I live. Even the housing market seems surprisingly solid where I am. Restaurants have been packed as usual. Neighbors buying new cars. I went to Atlantic City last weekend because I heard if you get some reward cards you can now get free rooms even on weekends – because their traffic is down (Trump Casinos bankrupt now for the 3rd time, surprise). Borgata had a 1000 person poker room with every seat filled and a waiting list to play.

Right now we have a bad recession, but its no worse than other recessions of the last few decades. And even the recession is probably going to end this year. So the way I see it, we are sort of entering a “calm before the storm” period where we will start to get some incremental improvements in economic numbers and the stimulus spending encourages more confidence. Just when people start to believe things are getting better and a market rally has sucked as many people as possible in, and VIX/VXO are back below 20 – well, you’ll know what to do... because we’ll soon after be back in recession and people will realize the stimulus plans are not enough. That’s when the real devastation will happen.

-

9_eU4oMpoNP

- Posts: 13

- Joined: Mon Oct 27, 2008 6:09 pm

Re: Financial topics

As I write this, the Dow (DJIA) is at 7,277.50. That's below the low from Oct. 9, 2002 (the bottom of the last recession). You have to go back to 1997 to find a Dow this low. We've just witnessed the loss of 12 years of gains in the Dow.

Re: Kaplan thinks we are due for major move higher

Gordo wrote:he already has a bike, muscle car, new hot tub, new

> hardwood floors, new 52" TV, all new guitar collection....all of it

> financed (He probably makes $60k and has no savings- and he's not a

> dumb guy at all).

Not a "dumb guy at all". "No savings", "finances everything" and "makes 60k a year".

Not sure what your friends definition of dumb is, but sounds like a "dumb guy" to me (I'm not criticizing how much he makes a year, just how much he spends vs. how much he makes).

Gordo wrote:I see the same sort of thing. If (when?) everyone really cuts back, that’s when the economy truly goes to hell in a hand basket. I don’t see this happening right now at all where I live. Even the housing market seems surprisingly solid where I am. Restaurants have been packed as usual. Neighbors buying new cars. I went to Atlantic City last weekend because I heard if you get some reward cards you can now get free rooms even on weekends – because their traffic is down (Trump Casinos bankrupt now for the 3rd time, surprise). Borgata had a 1000 person poker room with every seat filled and a waiting list to play.

Surely you believe the auto industry numbers being released lately right? Where even Toyota is cutting back big time due to demand.

Things don't happen over night. It's going to take some time. What is clear is that the "credit spigot" has largely been turned off (which is exactly what has been driving western economies for many years now).

Annicdotal evidence is not that reliable, as I'm sure you know. There's always the exception to the rule and some people respond by buying things to alleviate the stress of their lives.

I'm sure there will be a counter up swing bounce after a few week\months. The DIJA may go down to 6000 or so and then I'd expect a large counter rally (to 10,000?) that may last months and then back down to 3000 or possibly even lower.

As investor mood swings from one extreme to the other (fear to euphoria [and back to fear]), the market will react in the same manner. Some will interprit such action as a rally and get back in, but that euphoria wil be short lived (and so will their investments).

Good luck playing that game, it'll be like catching a "falling knife". Either way the overall market direction will be down for some time to come (and likely way down).

For those believing in going long, the next few years are likely going to turn that belief on it's head (as many companies are not sufficiently capitalized to survive the long term!)

Tobyguy

Last edited by tobyguy on Fri Feb 20, 2009 7:10 pm, edited 1 time in total.

CNBC Earnings Central Stats As of Friday, February 20th

EARNINGS STATS: BY THE NUMBERS

As of Friday, February 20th:

The blended earnings growth rate for the S&P 500 for Q4 2008,

combining actual numbers for companies that have reported, and

estimates for companies yet to report, stands at -42.1%, and if it

holds it will be the lowest earnings growth reate since Thomson

Reuters began tracking earnings growth rates in 1998. On July 1st, the

estimated growth rate for Q4 was 59.3%, and by October 1st, the

estimated growth rate had fallen to 46.7%. (Data provided by Thomson

Reuters)

Date 4Q Earnings growth estimate as of that date

------- -------------------------------------------

Feb 6: 50.0%

Jul 1: 59.3% Start of previous (3rd) quarter

Oct 1: 46.7% Start of quarter

Dec 5: 10.0%

Dec 12: 5.9%

Dec 19: 0.5%

Dec 26: -0.9% End of quarter

Jan 2: -1.2%

Jan 9: -15.1%

Jan 16: -20.2%

Jan 23: -28.1%

Jan 30: -35.2%

Feb 6: -40.6%

Feb 13: -42.1%

Feb 20: -42.1%

http://www.cnbc.com/id/15839135/site/14081545/

As of Friday, February 20th:

The blended earnings growth rate for the S&P 500 for Q4 2008,

combining actual numbers for companies that have reported, and

estimates for companies yet to report, stands at -42.1%, and if it

holds it will be the lowest earnings growth reate since Thomson

Reuters began tracking earnings growth rates in 1998. On July 1st, the

estimated growth rate for Q4 was 59.3%, and by October 1st, the

estimated growth rate had fallen to 46.7%. (Data provided by Thomson

Reuters)

Date 4Q Earnings growth estimate as of that date

------- -------------------------------------------

Feb 6: 50.0%

Jul 1: 59.3% Start of previous (3rd) quarter

Oct 1: 46.7% Start of quarter

Dec 5: 10.0%

Dec 12: 5.9%

Dec 19: 0.5%

Dec 26: -0.9% End of quarter

Jan 2: -1.2%

Jan 9: -15.1%

Jan 16: -20.2%

Jan 23: -28.1%

Jan 30: -35.2%

Feb 6: -40.6%

Feb 13: -42.1%

Feb 20: -42.1%

http://www.cnbc.com/id/15839135/site/14081545/

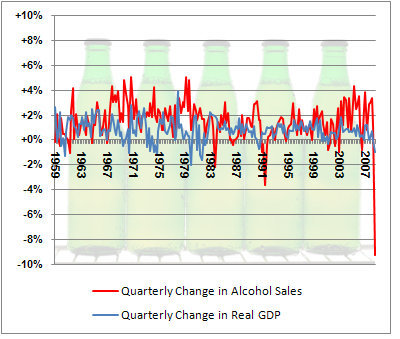

Re: Financial topics

Matt,

That's an incredibly interesting graph. If anything, I would think alcohol sales would be WAY UP given the market conditions! Alcohol producers should have more in sales than WalMart!

Rube

That's an incredibly interesting graph. If anything, I would think alcohol sales would be WAY UP given the market conditions! Alcohol producers should have more in sales than WalMart!

Rube

That inflationary bull market is laughable

Money don't come out of anything. The buyer pays no more than the seller. I think I saw 10 year treasuries were around 2.75% today, which is a full 1% lower than they generally were in the 2002-2003 bottom. We are early into this bear market. Remember, the last one lasted 3 years and there wasn't any real financial damage that time. You can't get money out of stocks and put it into bonds or money market accounts or anything on a net basis, that is an idiots accounting rule that they use in the press, but unless money is being borrowed for the purpose of buying bonds or stocks, it can't come out of anything. There isn't any money on the sidelines, that is a lie made up in the minds of children.

The world hasn't quit speculating and I suspect the gold and silver rush is nothing but another dotbomb game. Also, I suspect that people in Europe are really nervous and this is where they are going. For one, silver ins't a precious metal. YOu don't make forks and spoons out of precious metals. It is headed in the opposite direction of copper, which is an industrial metal just like silver. Plus, the real big uses of silver are flat on their butts, photography and electronics. If you think it is precious, put $100,000 worth on your back and run for the hills. Unless you are a young Arnold Swartzenager, the only way it gets on your back is if you are flat on your face. Oil isn't basing, but is being speculated all the way down. We are headed for a 20% decline in consumption is my best guess.

I don't believe Johns crash is going to happen because I believe it already happened. Stocks fell 4000 points in 6 weeks back in September/October. I think that was a crash. Also, the Nasdaq fell 40% in 2 weeks back in 2000. We have had plenty of crashes in the last 10 years. History has shown that markets like this grind down over a period of years, not in a crash. Japan has now been grinding down for 19 years and I don't believe it is finished. We could have a crash, but I think most people are resigned to staying the course because they have lost too much. It is the psychology of sitting in the casino until you are down to enough money to eat. Like the gold bulls, they will have to take what the market will pay when they have to sell. Sub 3000 is a minimum target on the Dow and I suspect we could go under 1000. I was asked what to do by a woman over 70 years old who had inherited a good amount of stock and money from her parents. She had a lot of oil stocks, COP, XOM and CVX. I told her to ask herself if she could stand for them to go to $10 and she about dropped the phone. Then I told her to look at what these stocks were selling for in 1990 because I had held to the belief that the bargains they were pushing in the financials would fall at a minimum to early 1990's prices and I was right. I don't believe they are done either, but the belief was based on the idea that all the schemes to increase lending since 1990 had collapsed and thus everything on top of 1990 would be wiped out. I believe now that the financial capital base has been wiped out to that level, the rest of the asset price base is going to follow. You might check what the Dow was in 1990? 2300 is my memory. Don't laugh, the Nikkei is trading at 1983 prices and it peaked in 1990.

I am working on some ideas about deflation. The government is destroying the economy to keep the economy from falling apart and correcting itself. This sounds absurd, but the economy will repair itself even though it will wipe out plenty of really rich people, maybe even the Warren Buffets of the world. But, if we keep fooling around with what they are doing right now, we are going to be in this mess for 30 years or more. My best guess is the way you heal a deflation, which is nothing but a natural mathematical response to too much and long a period of debt and asset inflation is through tight credit and low interest rates. This is somewhat akin to what Mr. Koo of the JCB said, except it is going to have to be a closer balance budget and probably higher taxes as well over the long term. I don't like socialist ideas, but this is a socialist problem we have, not a free market problem. The money supply naturally falls from debt repayment and we are in situation where piling up government debt isn't going to fix this one. The Japanese tried it and it didn't work. There isn't going to be a US inflating the world this time around to allow for excess cash flow for governments to do what Japan did. In any case, not one person in the world can point to Japan and say they fixed their problem. The only way we inflate this is to deflate it. If they inflate this game, it will collapse.

The world hasn't quit speculating and I suspect the gold and silver rush is nothing but another dotbomb game. Also, I suspect that people in Europe are really nervous and this is where they are going. For one, silver ins't a precious metal. YOu don't make forks and spoons out of precious metals. It is headed in the opposite direction of copper, which is an industrial metal just like silver. Plus, the real big uses of silver are flat on their butts, photography and electronics. If you think it is precious, put $100,000 worth on your back and run for the hills. Unless you are a young Arnold Swartzenager, the only way it gets on your back is if you are flat on your face. Oil isn't basing, but is being speculated all the way down. We are headed for a 20% decline in consumption is my best guess.

I don't believe Johns crash is going to happen because I believe it already happened. Stocks fell 4000 points in 6 weeks back in September/October. I think that was a crash. Also, the Nasdaq fell 40% in 2 weeks back in 2000. We have had plenty of crashes in the last 10 years. History has shown that markets like this grind down over a period of years, not in a crash. Japan has now been grinding down for 19 years and I don't believe it is finished. We could have a crash, but I think most people are resigned to staying the course because they have lost too much. It is the psychology of sitting in the casino until you are down to enough money to eat. Like the gold bulls, they will have to take what the market will pay when they have to sell. Sub 3000 is a minimum target on the Dow and I suspect we could go under 1000. I was asked what to do by a woman over 70 years old who had inherited a good amount of stock and money from her parents. She had a lot of oil stocks, COP, XOM and CVX. I told her to ask herself if she could stand for them to go to $10 and she about dropped the phone. Then I told her to look at what these stocks were selling for in 1990 because I had held to the belief that the bargains they were pushing in the financials would fall at a minimum to early 1990's prices and I was right. I don't believe they are done either, but the belief was based on the idea that all the schemes to increase lending since 1990 had collapsed and thus everything on top of 1990 would be wiped out. I believe now that the financial capital base has been wiped out to that level, the rest of the asset price base is going to follow. You might check what the Dow was in 1990? 2300 is my memory. Don't laugh, the Nikkei is trading at 1983 prices and it peaked in 1990.

I am working on some ideas about deflation. The government is destroying the economy to keep the economy from falling apart and correcting itself. This sounds absurd, but the economy will repair itself even though it will wipe out plenty of really rich people, maybe even the Warren Buffets of the world. But, if we keep fooling around with what they are doing right now, we are going to be in this mess for 30 years or more. My best guess is the way you heal a deflation, which is nothing but a natural mathematical response to too much and long a period of debt and asset inflation is through tight credit and low interest rates. This is somewhat akin to what Mr. Koo of the JCB said, except it is going to have to be a closer balance budget and probably higher taxes as well over the long term. I don't like socialist ideas, but this is a socialist problem we have, not a free market problem. The money supply naturally falls from debt repayment and we are in situation where piling up government debt isn't going to fix this one. The Japanese tried it and it didn't work. There isn't going to be a US inflating the world this time around to allow for excess cash flow for governments to do what Japan did. In any case, not one person in the world can point to Japan and say they fixed their problem. The only way we inflate this is to deflate it. If they inflate this game, it will collapse.

Who is online

Users browsing this forum: Google [Bot], Majestic-12 [Bot] and 40 guests